(Bloomberg) — The yen has slumped to a level that leaves it on track for its worst year on record, prompting the strongest warnings to date from senior Japanese government officials aimed at stemming the slide.

(Bloomberg) — The yen has slumped to a level that leaves it on track for its worst year on record, prompting the strongest warnings to date from senior Japanese government officials aimed at stemming the slide.

The currency fell as much as 1.5% to 144.99 per dollar Wednesday, coming within a whisker’s reach to 145 per dollar. It is the yen’s third day of declines as a fresh wave of dollar strength ripped through Asia and beyond, putting pressure on a range of foreign exchange markets.

Finance Minister Shunichi Suzuki said he was concerned about very sudden and one-sided moves in the currency market, following on from earlier comments by the government’s top spokesman.

“We’ll keep watching the markets with a high sense of urgency, and if the moves continue we’ll respond as needed,” he said. Suzuki declined to specify what action he might take amid speculation the government might eventually have to step into markets if the slide continues.

“The necessary response is the necessary response,” he said.

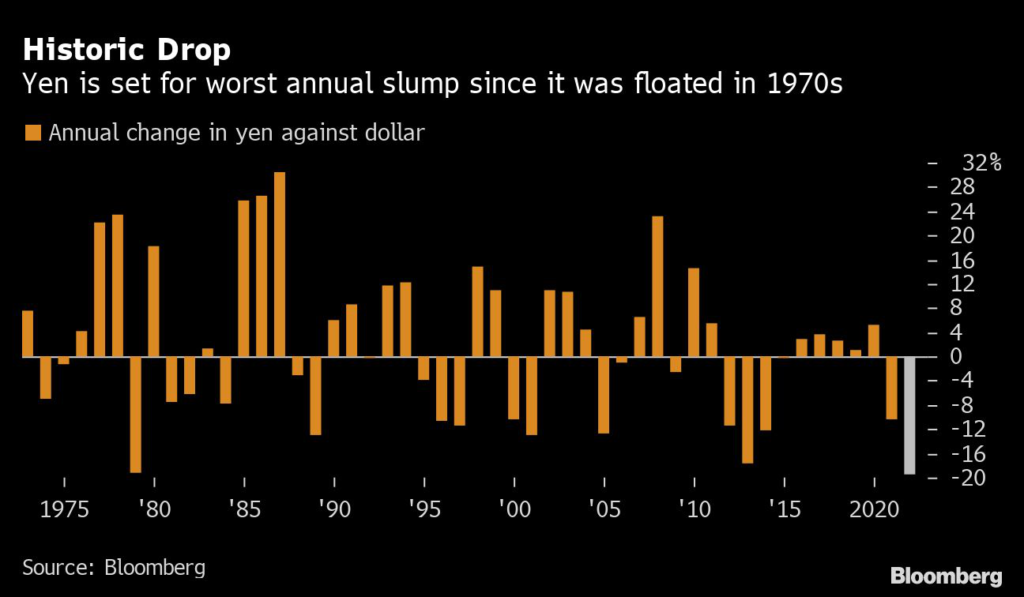

Japan’s currency has slumped 20% this year, and fell past its previous worst annual drawdown in 1979. The renewed selloff in Treasuries this month has widened the yield gap between the US and Japan, driving up the dollar and pushing the yen to a 24-year low.

Despite the salvo of official warnings on Wednesday, the comments were insufficient to reverse the yen’s slide in the face of intense dollar strength.

The US Treasury Department on Wednesday was also reluctant to suggest any potential intervention into currency markets to halt the yen’s depreciation with Treasury spokesman Michael Gwin saying the department had nothing new to add to Secretary Janet Yellen’s July stance. She had commented at that time the Treasury’s view “is that countries like Japan, the United States, the G-7 countries, should have market-determined exchange rates.” Later that month she added, after a meeting with Japanese Finance Minister Shunichi Suzuki, “only in rare and exceptional circumstances is intervention warranted and we did not discuss intervention.”

Traders are expecting a sturdier ramping up of language or the calling of a three-way meeting between the Bank of Japan, finance ministry and financial regulator in response to the recent sharp slide.

“While the tone of verbal intervention has become a bit stronger, market sensitivity may be falling as focus now is whether there will be an actual intervention,” said Teppei Ino, head of global markets research at MUFG Bank Ltd. “A stronger tone of the verbal intervention or an actual trilateral meeting of the BOJ, the MOF and the FSA are more important for the markets.”

Pressure On

Dollar-yen’s surge past the 144 level for the first time since 1998 will ramp up pressure on BOJ Governor Haruhiko Kuroda’s defiance of a global shift toward rate hikes, and the strength of Prime Minister Fumio Kishida’s support for his stance.

“The MOF and the BOJ probably believe the current phase is clearly the dollar’s strength, and not the yen’s issue,” said Mari Iwashita, chief market economist at Daiwa Securities Co. “That means there unfortunately is no sense of urgency about intervention or the need for the BOJ to tweak policy.”

In June, Japanese officials said they would take action if necessary, without specifying what that would be, after a three-party meeting held between the Ministry of Finance, the central bank and the Financial Services Agency.

A Trader’s Guide to Japanese Policy Makers’ Language on the Yen

Japan last intervened to prop up the currency in 1998, at around the same time much of Asia was being buffeted by a regional financial crisis.

Kuroda has repeatedly said that foreign exchange policy is the remit of the finance ministry, not the BOJ, while standing his ground on keeping rock-bottom interest rates to support the economy and generate a more stable form of inflation. He has insisted that a policy tweak to turn the currency tide would be largely futile anyway.

“I think Kuroda is right in that a small rate hike by the BOJ won’t stop the trend,” said Harumi Taguchi, principal economist at S&P Global Market Intelligence.

Beyond offering more help against rising prices fueled by the yen, the options are also limited for the government, she added. “Japan can only intervene unilaterally in foreign exchange, which won’t reverse the trend beyond a one-off shock.”

The yen is seen as one of the most important demarcations of how close the BOJ is to shifting its policy, according to Deutsche Bank AG’s chief international strategist Alan Ruskin. “Implicitly, every time the yen weakens, it asks the BOJ a question, as to whether now is the time to abandon YCC,” he wrote in a note dated Tuesday, referring to the central bank’s yield curve-control policy. “When nothing more than verbal intervention is at hand, the market can read from the lip service that the authorities are still some way from tightening monetary policy.”

Bond Purchases

In the bond market Wednesday, the BOJ said it would boost scheduled debt purchases as the intensifying Treasuries selloff also put upward pressure on yields. The move came as Japan’s benchmark 10-year yield approached the 0.25% upper limit of the BOJ’s tolerated trading band.

In the options market, bets on further yen weakness are growing. One-year risk-reversals for dollar-yen — a gauge of expected direction for the currency pair over that time frame — have hit the highest since 2015, according to data compiled by Bloomberg.

“So long as US bond yields are rising, which they are right now, and if the BOJ is trying to maintain this 25 basis point target on the 10-year JGB, the yen’s going to keep going down,” Chris Wood, global head of equity strategy at Jefferies, said on Bloomberg TV. “The fundamental cause of the collapse of the yen this year is the stubborn commitment by the BOJ governor to this yield-curve control policy.”

(Updates pricing information and adds quotes throughout.)

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.