(Bloomberg) — Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

(Bloomberg) — Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

Wall Street is looking for clues on any reduction in the European Central Bank’s bond reinvestments when officials gather this week.

Strategists at Bank of America, Morgan Stanley and Citigroup are on alert for hints over so-called quantitative tightening as policy makers prepare to increase borrowing costs for a second meeting.

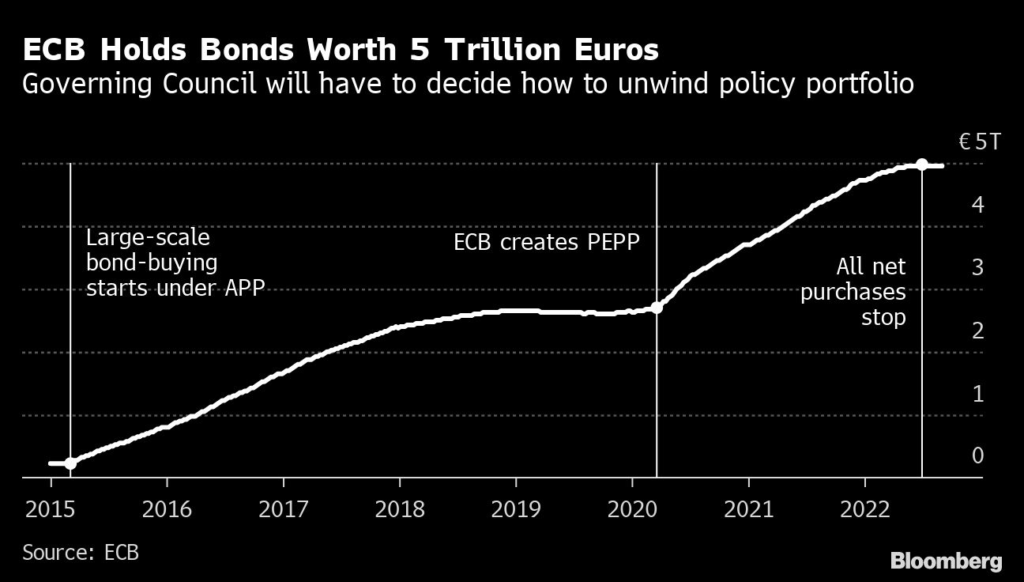

While trimming the ECB’s 5 trillion-euro ($5 trillion) bond holdings risks blowing out spreads in the region’s periphery, continued reinvestment threatens to further stoke price pressure and runs counter to efforts to wind-down monetary stimulus.

“Continuing with interest-rate hikes while not signaling a move to stop the expansion of the ECB balance sheet is not a credible policy mix,” said Rob Robis, chief global fixed income strategist at BCA Research, who expects an announcement this week. “The ECB Governing Council understands that they need to signal a credible monetary policy response to the euro-area inflation overshoot.”

Consumers in the 19-nation region are seeing prices rising at an annual rate of just under 10%, with the peak potentially still months away. QT — the logical next step in central bank efforts to unwind crisis-era stimulus — hasn’t been much of a topic in the euro zone, though some officials have argued that it’s an issue that’ll have to be discussed before long.

The Federal Reverse, ahead of the ECB in raising interest rates, is already ramping up efforts to unwind its $9 trillion portfolio. The Bank of England has also laid out plans to sell its holdings of UK government bonds.

At the ECB, QT is complicated by concerns that national bond markets react differently to shifts in monetary policy. Only seven weeks ago, officials presented a new purchase program to ensure changes are transmitted smoothly into all corners of the bloc.

That’s why the ECB’s efforts will likely concentrate on its 3.3 trillion-euro holdings bought under the Asset Purchase Program that started in earnest in 2015 and was aimed at shielding the euro zone from deflation.

A commitment to keep reinvestments under the more flexible Pandemic Emergency Purchase Program running through at least 2024 is unlikely to change given it’s the institution’s first line of defense against unwarranted jumps in borrowing costs for weaker euro-zone countries.

Recession Scenario

The extra yield investors demand to hold Italy’s 10-year notes over similar German bonds was around 235 basis points on Wednesday, close to the highest levels seen this year and up from a recent low of 181 basis points in July.

The spread is likely to widen as Italy faces an election this month, with prospects of a government led by Giorgia Meloni, whose party’s post-fascist roots have unsettled investors. The euro region’s increasingly cloudy economic outlook and reduced ECB support — either via higher rates or lower reinvestments — may widen the gap further.

“Europe is going into a recession as a baseline scenario,” said Annalisa Piazza, fixed income research analyst, MFS Investment Management. “Asset sales would be completely inconsistent with the view that re-investments are needed to help in case of fragmentation.”

It’s a view shared by strategists at Citi, who argue that ending APP reinvestments is “contradictory.” The Governing Council hasn’t formally discussed QT though staff economists are currently studying efforts by the Fed and the BOE to see if they hold any clues to what any ECB’s strategy should look like.

“Silence about QT has been massive and suggests policy makers are struggling to figure out how to actually pull it off,” said Anatoli Annenkov, a senior economist at Societe Generale.

Discussions can begin on shrinking the balance sheet though action isn’t needed now, Latvian central-bank chief Martins Kazaks — a more hawkish official — said in a recent Bloomberg interview. His Finnish colleague Olli Rehn — a policy dove — argued it’s premature to start talking publicly about QT.

“Looking at financial conditions, there’s not a big case for it at this point in time but of course it’s part of the playbook,” said ABN Amro’s Nick Kounis. “I’m also not convinced about what the narrative would be. The simple one is inflation is too high and we need to throw everything at it. But if you think about how QT will actually affect the inflation outlook, the case is less convincing.”

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.